In boardrooms across Australia, a seismic shift is occurring. The new Australian Sustainability Reporting Standards (ASRS) represent a significant change to corporate reporting requirements, with far-reaching implications for how businesses measure, manage, and disclose their environmental impact.

For CEOs, CFOs, Heads of Sustainability and Legal departments at Australia’s largest companies, this isn’t just another compliance checkbox—it’s a fundamental transformation of how business performance is measured and reported. The stakes are high: non-compliance risks significant penalties, reputational damage, and investor scrutiny. The clock is ticking for businesses to get up to speed on their reporting requirements under the new standards and the process is anything but simple.

To help businesses understand their responsibilities and prepare for reporting we’ve broken down the complex new reporting requirements into a clear, actionable plan that will help to reduce the overwhelm. In this guide you’ll gain a thorough understanding of the ASRS scope, timelines, and implications for your business, equipping you with the knowledge needed to comply with ease and confidence.

Australian Sustainability Reporting Standards deep dive

Background

The ASRS are broken down into two main reporting standards – AASB S1 which is voluntary and AASB S2 which is mandatory.

From January 1 2025, mandatory climate reporting (AASB S2) came into effect and requires businesses of a certain size to assess and disclose information about their climate-related risks and opportunities in a ‘Sustainability Report’. The Sustainability Report should be included in a business’s annual financial report. The introduction of AASB S2 marks Australia’s alignment with existing international frameworks, particularly the International Sustainability Standards Board (ISSB) standards, while addressing the specific needs of the Australian market.

The move to mandatory climate reporting was prompted by increasing pressure from investors, consumers, and international regulatory bodies for comprehensive, comparable sustainability data. Prior to this, sustainability reporting in Australia was largely voluntary, resulting in inconsistent disclosure practices across companies and sectors. The new mandatory framework aims to standardise these practices, ensuring that stakeholders have access to reliable information about a company’s sustainability performance and how it impacts overall financial risks, opportunities and performance.

Scope and context

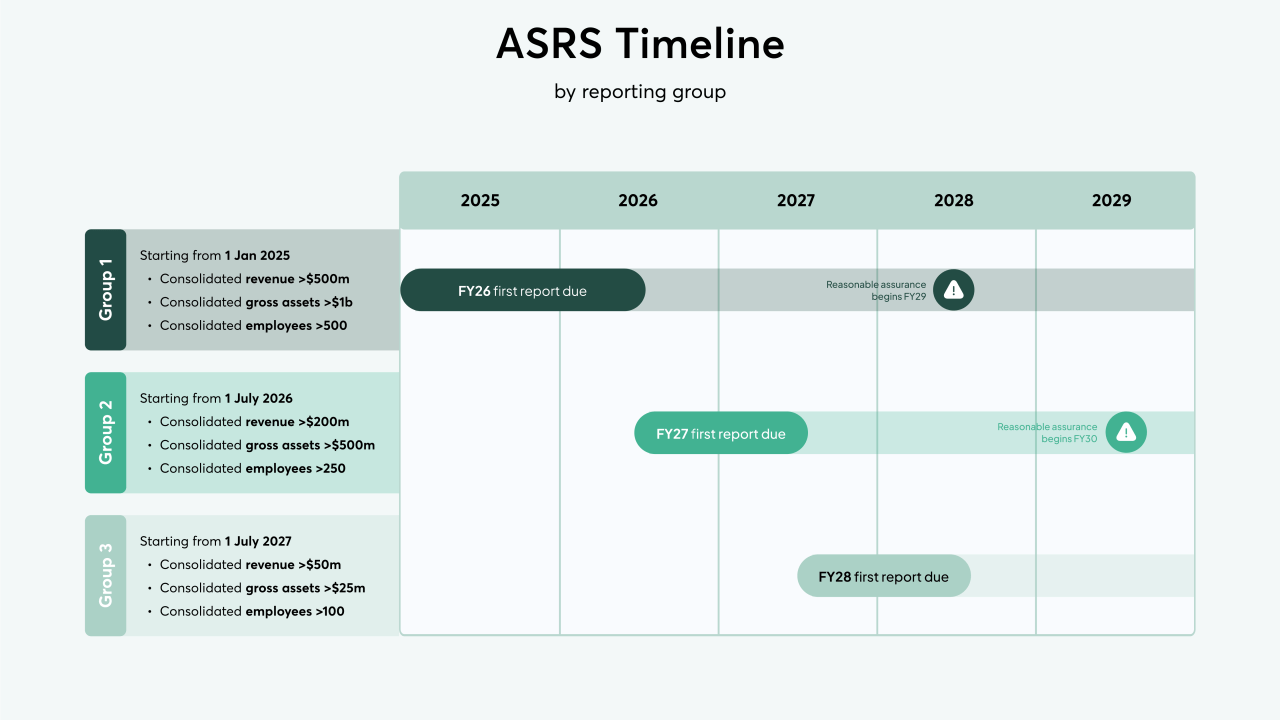

AASB S2 applies to Australian companies in three distinct groups. A business qualifies for a group if they meet two out of three of the below criteria;

Group 1 entities:

- More than 500 employees

- Annual revenue exceeding $500 million

- Consolidated assets over $1 billion

Group 2 entities:

- More than 250 employees

- Annual revenue exceeding $200 million

- Consolidated assets over $500 million

Group 3 entities:

- More than 100 employees

- Annual revenue exceeding $50 million

- Consolidated assets over $25 million

Note: there are a couple of exceptions to these groups depending on whether businesses are registered under the NGER Act or part of other registered schemes, RSEs or retail CCIVs. For more information refer to the table on page 13 of ASIC’s Regulatory Guide

This tiered approach recognises that larger organisations generally have greater impacts under the standards and more resources available for reporting. AASB S2 covers both Australian public companies and large proprietary companies meeting these thresholds.

In an international context, Australia’s approach parallels developments in other jurisdictions, such as the European Union’s Corporate Sustainability Reporting Directive (CSRD). However, Australia’s framework incorporates unique elements addressing our specific national circumstances, including considerations related to natural resource industries that form a significant portion of the economy.

Key elements of AASB S2

AASB S2 requires businesses to report disclosures across five key areas:

- Governance

- How the board and management team oversees and manages climate-related risks and opportunities

- In what ways climate considerations are integrated into existing governance processes and structures

- Business strategy

- Set out how climate-related risks and opportunities impact the business model, strategy, financial planning and performance of the business

- The resilience of the business to withstand varying climate scenarios

- Plans for the business to adapt to climate-related risks and opportunities, transition to the lower-carbon economy, and any targets that have been set

- Risk management

- Detail the processes used to identify, assess and manage climate-related risks

- How these processes will be integrated into the broader risk management framework

- Metrics and targets

- Disclosure of climate-related metrics and performance indicators

- Measurement of Scope 1, 2 and 3 greenhouse gas (GHG) emissions

- Climate targets (e.g. net zero commitments) and the business’s progress towards their achievement

- Assurance

- Businesses must obtain assurance for their climate reporting and adhere to the defined assurance timeline. Find more information on what type of assurance is required for mandatory climate reporting and the timeline here.

Roles and responsibilities

AASB S2 creates new responsibilities across multiple corporate functions:

Board and C-Suite:

- Ultimate accountability for sustainability reporting

- Setting the tone for the organisation’s approach to sustainability

- Approving sustainability disclosures and ensuring their accuracy

CFO and finance team:

- Integrating sustainability considerations into financial planning and reporting

- Developing systems for collecting and verifying sustainability data

- Ensuring consistency between financial and sustainability disclosures

Head of Sustainability:

- Leading the development of sustainability strategies and reporting processes

- Coordinating cross-functional sustainability initiatives

- Staying abreast of evolving sustainability standards and best practices

General Counsel and legal team:

- Interpreting regulatory requirements and advising on compliance

- Reviewing sustainability disclosures for legal risks

- Managing potential litigation related to sustainability claims

CTO and technology team:

- Implementing systems for collecting, managing, and reporting sustainability data

- Ensuring data security and integrity

- Developing analytics capabilities for sustainability performance

Timelines

AASB S2 includes a phased implementation approach:

Group 1 entities:

- Preparatory period: 2023-2024

- First reporting year: Financial year beginning on or after January 1, 2025

- First reports due: Within 4 months of the end of the financial year

Group 2 entities:

- Preparatory period: 2024-2026

- First reporting year: Financial year beginning on or after July 1, 2026

- First reports due: Within 4 months of the end of the financial year

Group 3 entities:

- Preparatory period: 2025-2027

- First reporting year: Financial year beginning on or after July 1, 2027

- First reports due: Within 4 months of the end of the financial year

This staggered timeline acknowledges the significant preparation required, particularly for organisations new to mandatory climate reporting.

Why this matters to your business

The new reporting requirements represent both significant risks and strategic opportunities for affected businesses:

Risks

Compliance risks:

- Financial penalties for non-compliance or misleading disclosures

- Regulatory investigations and enforcement actions

- Potential director liability issues

Reputational risks:

- Investor scrutiny of sustainability performance and targets

- Consumer backlash against perceived greenwashing

- Competitive disadvantage when compared to sustainability leaders

Operational risks:

- Exposure of inefficiencies in resource usage and waste management

- Identification of vulnerable supply chain dependencies

- Identification of climate risk exposure previously not fully understood

Financial risks:

- Potential for higher cost of capital if sustainability performance lags

- Asset valuation impacts due to climate transition risks

- Investment constraints from sustainability-focused investors

Business process changes

AASB S2 will necessitate fundamental changes to how businesses operate:

Data collection and management:

- New systems will be required for collecting, validating, and storing sustainability data (including the emissions data of your business and its value chain)

- New sources of data must be captured e.g. operational and value chain data.

- Cross-functional data collection will be required given sustainability disclosures are not siloed in sustainability teams only.

Governance structures:

- Creation of new sustainability committees at a board level

- New reporting lines and accountability mechanisms

- Adoption of sustainability governance best practices

Strategic planning:

- Incorporating climate scenarios into long-term planning

- Reassessment of capital allocation priorities

- Supply chain reorganisation based on sustainability criteria

External communications:

- More detailed sustainability disclosures in annual reports

- Enhanced investor communications regarding sustainability strategies and performance

- Coordinated messaging across all sustainability-related disclosures

Key challenges

Organisations face several significant challenges in implementing the new reporting requirements:

Data quality and availability

Many companies lack robust systems and processes for collecting comprehensive sustainability data, particularly for Scope 3 emissions that occur throughout the value chain. Historical data may be incomplete or inconsistent, making it difficult to establish baselines and track progress. The requirement to report with the same rigor as financial information necessitates investment in new data collection processes and verification mechanisms.

Technical expertise

The specialised knowledge required for climate risk assessment, emissions calculation, and scenario analysis is often in short supply. Many organisations lack personnel with the necessary skills to implement the legislation’s requirements effectively. This expertise gap can lead to delays, errors, and compliance issues if not addressed quickly and proactively.

Cost and resource allocation

Implementing comprehensive sustainability reporting systems can require significant investment in technology, consulting services, and personnel. For Group 2 companies in particular, these costs may represent a substantial burden. Balancing these investments against other business priorities is a challenging trade-off for leadership teams.

Alignment with existing systems

Integrating sustainability reporting with established financial reporting processes requires careful coordination. Differences in reporting cycles, data sources, and verification procedures can create friction and inefficiencies. Companies must consider how to reconcile these differences while maintaining the integrity of both reporting streams.

Managing stakeholder expectations

Different stakeholders may have divergent expectations regarding sustainability disclosures. Investors might focus on financial materiality, while customers and employees may be concerned with broader impacts. Balancing these expectations while complying with regulatory requirements demands sophisticated stakeholder management.

Key opportunities

Despite the challenges, the new standards create significant opportunities for forward-thinking organisations:

Operational efficiency

The process of collecting and analysing sustainability data often reveals inefficiencies in resource usage, energy consumption, and waste management. Addressing these inefficiencies can yield substantial cost savings while reducing environmental impact. Similarly, adopting innovative technologies to manage compliance requirements can streamline your processes and reduce the need for specialised in-house expertise resulting in further cost savings.

Enhanced risk management

Systematic assessment of climate-related risks improves overall enterprise risk management. Organisations will gain better visibility into physical risks (such as facility exposure to extreme weather) and transition risks (such as policy changes affecting carbon-intensive assets) through the process of mandatory climate reporting.

Access to sustainable finance

Companies with robust sustainability reporting and strong performance can access growing pools of sustainable finance, including green bonds and sustainability-linked loans that may offer preferential terms. This can lower the overall cost of capital, make resource allocation easier and diversify funding sources.

AI driven systems and processes

Companies that take an innovative approach to data collection by using AI and automation will see improvements in data accuracy and granularity, resulting in a more efficient, cost effective and streamlined reporting process.

Improved investor relations

Comprehensive sustainability disclosures can provide investors with the information they increasingly demand for decision-making. This transparency can attract long-term, stable investors aligned with the company’s sustainability vision, potentially reducing share price volatility.

Case study: Fortescue Metals Group’s climate response

Fortescue Metals Group (FMG), one of Australia’s largest mining companies, provides an instructive example of proactive adaptation to enhanced climate reporting requirements.

In anticipation of stricter reporting standards, FMG established its Climate Change Strategy in 2020, committing to net zero operational emissions by 2040—a bold target for a company in an emissions-intensive industry. The company backed this commitment with a $6.2 billion investment in decarbonisation initiatives.

Key Components of FMG’s Approach:

- Integrated reporting structure: FMG reorganised its reporting systems to integrate sustainability data collection with financial reporting processes, ensuring consistent data quality and timely disclosure.

- Board-level oversight: The company established a Sustainability Committee at the board level, chaired by an independent director with climate expertise, demonstrating governance best practices.

- Technology deployment: FMG invested in advanced data management systems to track emissions across operations and supply chains, enabling more accurate and comprehensive disclosures.

- Strategic pivot: Beyond compliance, FMG launched Fortescue Future Industries to develop green hydrogen and renewable energy projects, positioning the company for growth in the low-carbon economy.

- Stakeholder engagement: The company implemented a comprehensive stakeholder engagement program to explain its climate strategy and gather feedback, enhancing transparency and building trust.

Results:

- 25% reduction in emissions intensity between 2020 and 2023

- Above average analyst ratings of 66/100 for climate risk management

- Successful issuance of a $1.5 billion sustainability-linked bond at competitive rates

- Enhanced relationships with key customers seeking low-carbon materials. A notable example is FMG’s active engagement with its customers in China, Japan, and South Korea—major markets for its iron ore—to develop and adopt low-carbon steel production technologies.

Key Learnings:

- Early action pays dividends: By anticipating regulatory changes, FMG gained a first-mover advantage and were well prepared for inevitable mandatory climate reporting requirements.

- Cross-functional teams are essential: Successful implementation requires collaboration across finance, operations, sustainability, and legal departments.

- Technology investment is crucial: New data management systems are fundamental to effective reporting and streamlining complex processes. .

- Strategy integration delivers value: Climate considerations became part of core business strategy, not just a compliance exercise.

- Leadership commitment drives change: CEO and board-level commitment was crucial to meaningful implementation and having a coordinated approach that simplified the entire process.

This case study demonstrates that companies with a proactive approach to mandatory climate reporting can create significant value for shareholders while reducing the burden of compliance on their entire organisation.

Next steps

For organisations subject to mandatory climate reporting, there are a few key next steps that can help you understand your reporting requirements and prepare well ahead of your first reporting season.

- Conduct a readiness assessment:

- Evaluate current sustainability reporting capabilities

- Identify gaps in data collection, systems, and expertise

- Develop a prioritised action plan addressing critical gaps

Information on how to conduct readiness assessments is covered in Chapter 2 of Greener Academy

- Establish governance structures:

- Define board and executive oversight responsibilities

- Create cross-functional working groups with clear mandates

- Develop approval processes for sustainability disclosures

- Prepare for auditing

- Understand what information will and will not be audited

- Ensure your climate disclosures and data align with the relevant auditing standards

- Strengthen internal controls and data governance to reduce gaps and improve accuracy and traceability

- Identify technology solutions that streamline data collection and increase auditability

A comprehensive guide to governance under AASB S2 is covered in Chapter 4 of the Greener Academy.

- Invest in systems and expertise:

- Implement or upgrade sustainability data management systems

- Recruit or develop specialised expertise in key areas

- Consider external partnerships for specialised capabilities

We breakdown how to leverage digital tools and new data processing technologies in Chapter 5 of the Greener Academy.

- Establish an emissions measurement strategy

- Identify emissions sources

- Implement measurement systems and tools

- Establish data quality controls

Get all the information you need to develop a comprehensive emissions measurement strategy in Chapter 3 of the Greener Academy.

- Perform climate risk and opportunity assessment:

- Identify material climate-related risks and opportunities

- Conduct scenario analysis for different climate futures

- Quantify potential financial impacts where possible

Find out how to conduct risk and opportunity analysis in Chapter 7 of the Greener Academy.

- Develop transition plans and targets:

- Set science-based emissions reduction targets

- Develop detailed roadmaps for achieving targets

- Align capital allocation with transition objectives

- Identify opportunities to reduce emissions and transition to lower carbon economy

- Develop roadmaps for transition and emissions reduction and allocate capital

- Set short, medium and long term targets, and track progress towards these targets

You can download a transition target setting template in Chapter 8 of the Greener Academy.

- Monitor evolving standards:

- Establish processes for tracking regulatory developments

- Participate in industry consultations where appropriate

- Build flexibility into reporting systems to accommodate changes

Check the Greener Academy page for quarterly regulatory updates that capture policy changes and new guidance from regulatory bodies.

- Integrate with strategic planning:

- Incorporate sustainability considerations into strategic reviews

- Align sustainability initiatives with business objectives

- Identify competitive advantages from sustainability leadership

By taking these steps, your organisation can not only achieve compliance with the new standards but potentially transform sustainability reporting from a regulatory obligation into a source of strategic advantage.

Additional reading

For deeper exploration of topics related to the new mandatory climate reporting standards, consider these resources:

- Commonwealth of Australia Treasury: “Mandatory Climate related financial disclosures: Policy statement”

- Australian Accounting Standards Board (AASB) and Auditing and Assurance Standards Board (AUASB) Joint Publication: “Climate-related and other emerging risk disclosures: assessing financial statement materiality”

- Australian Securities & Investments Commission: Regulatory Guidance on Sustainability